What is Reconciliation? Meaning, Steps, Statements & Automation

Reconciliation is the process of comparing two or more sets of records to confirm they match, identify differences, and correct errors. Businesses use reconciliation to verify balances, prevent fraud, improve reporting accuracy, and maintain compliance across bank accounts, ledgers, taxes, invoices, and operational systems.

When money moves through multiple systems, mismatches happen. A payment may appear in the bank but not in the ledger. A GST figure may differ from invoices. A customer credit note may sit in one ERP but not another. Reconciliation helps teams catch those gaps before they turn into bigger financial problems.

Think of it like syncing two watches. If they show different times, one of them is wrong – or both need adjustment. In business, those “watches” are systems, statements, and reports.

Why Reconciliation Matters in Modern Finance

The value of Reconciliation meaning goes far beyond a monthly accounting task. It is a control process that builds confidence in business data. Business leaders rely on numbers to make decisions on cash flow, profitability, taxes, and growth. If the numbers are wrong, the decisions become weaker from the start.

Many companies focus only on speed. They want a faster monthly closing. But here’s the thing – speed without accuracy creates hidden risks. A slower closing with clean data often works better than a fast close full of unresolved issues.

Reconciliation also helps reduce fraud and supports audits. The Association of Certified Fraud Examiners has reported that organizations lose an estimated 5% of annual revenue to fraud on average. Regular checks and reconciled records help reduce that exposure.

What is Reconciliation used for?

It is is used to detect errors, verify balances, prevent duplicate entries, reduce fraud risk, and support regulatory compliance. It gives finance teams confidence that the numbers used in reports, forecasts, and audits reflect the real position of the business. Furthermore, regular recon helps companies spot operational issues early, such as delayed payments, missing invoices, or system integration gaps. Better data leads to better decisions.

Why do companies do reconciliation every month?

Companies reconcile monthly because errors compound. A payment posted to the wrong account in January silently distorts every downstream report through December. Monthly cycles catch these issues before they cascade. Regulatory requirements – including those under GST, IND AS, and various GAAP standards – also mandate periodic reconciliation as part of compliant financial reporting.

What is reconciliation in accounting?

In accounting, reconciliation means comparing internal records with source documents, statements, or supporting schedules to confirm balances are accurate and complete.

It helps businesses identify:

- Missing entries

- Duplicate transactions

- Posting errors

- Timing differences

- Incorrect classifications

Common examples include matching general ledgers with bank statements, invoices, accounts receivable schedules, accounts payable balances, or tax records.

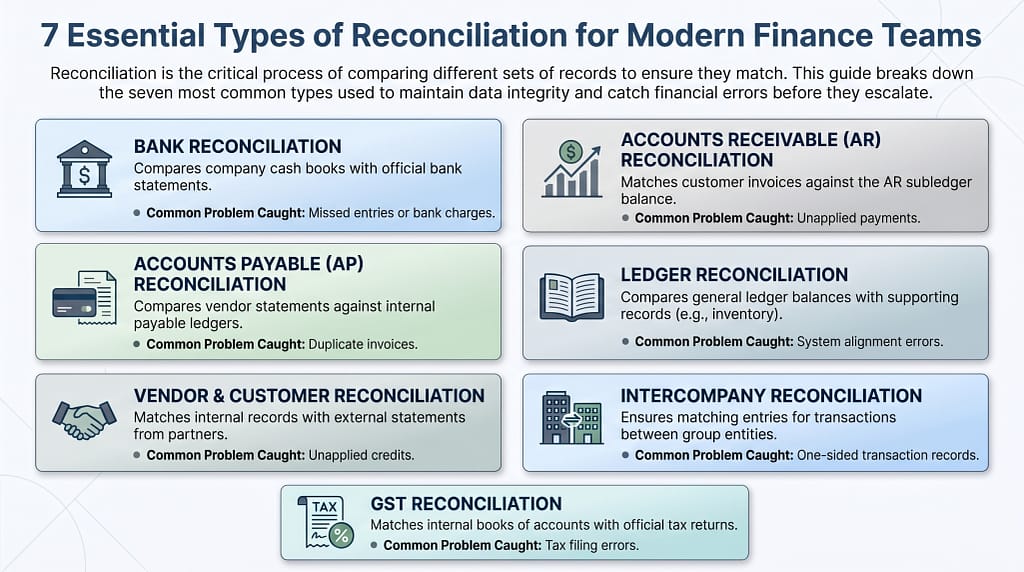

Types of Reconciliation Every Business Should Know

Different records require different checks. That is why businesses use multiple forms of Reconciliation depending on the process.

Bank Reconciliation

A Bank reconciliation statement compares the company cash book with the official bank statement. It explains differences such as outstanding cheques, deposits in transit, bank charges, or missed entries.

Because cash is critical, this is one of the most common and important reconciliation processes.

Accounts Receivable Reconciliation

Accounts Receivable Reconciliation matches the total of all open customer invoices against the AR subledger balance. Discrepancies often signal unapplied payments, credit notes not processed, or write-offs that slipped through approval.

Accounts Payable Reconciliation

Accounts Payable Reconciliation does the reverse – it compares vendor statements against internal payable ledgers. This catches duplicate invoices, missing credit memos, and payments applied to the wrong vendor account.

Ledger Reconciliation

Ledger reconciliation compares balances in the general ledger with supporting schedules such as receivables, payables, or inventory records. If numbers do not align, finance teams investigate the reason.

Vendor and Customer Reconciliation

This process compares internal records with supplier or customer statements. It helps identify missed invoices, short payments, duplicate payments, or unapplied credits.

Intercompany Reconciliation

Large groups with multiple entities often transact internally. Intercompany reconciliation ensures both sides of the same transaction record matching entries.

GST Reconciliation

GST reconciliation compares books of accounts with GST returns and tax data. It helps businesses claim the right credits and avoid filing errors. It involves matching sales, purchases, tax liability, and input tax credit data between business records and returns. Strong GST controls improve tax accuracy and lower compliance risk.

What is a Bank reconciliation statement?

A Bank reconciliation statement is a report that explains differences between a company’s cash records and the bank’s official statement for the same period. It usually includes outstanding cheques, deposits in transit, bank fees, interest credits, bounced payments, and missed entries in either record. The purpose is to adjust both sides logically until the balances align. Many businesses prepare this statement monthly, while high-volume companies may review it daily.

Is bank reconciliation the same as account reconciliation?

Bank reconciliation is a specific subset of account reconciliation. Account reconciliation refers to the broader process of verifying the balance of any general ledger account, while bank reconciliation specifically focuses on matching cash book balances with bank-issued statements. Both fall under the umbrella of what is reconciliation in accounting, but they address different ledger accounts and use different source documents

Step by Step Reconciliation Process:

Strong reconciliation follows a clear workflow. Without structure, teams waste time chasing avoidable errors.

1. Gather Source Data

Collect bank statements, ERP exports, invoices, ledgers, tax files, and transaction logs. Complete data matters because missing inputs create false mismatches.

2. Standardize Data

Dates, currencies, references, and naming formats often differ across systems. Teams first clean and standardize records before matching them.

Think of it like sorting puzzle pieces before building the picture.

3. Match Transactions

Compare records using rules such as exact amount, date range, invoice number, or customer ID. Modern tools can also use fuzzy matching when references vary slightly.

4. Investigate Exceptions

Review unmatched items carefully. Some issues come from timing delays. Others signal missing entries, duplicate payments, or human error.

5. Pass Corrections

Post journal entries, update records, or fix operational mistakes. Then rerun checks if needed.

6. Approve and Document

Store notes, approvals, and evidence. This creates a clear audit trail for internal teams and auditors.

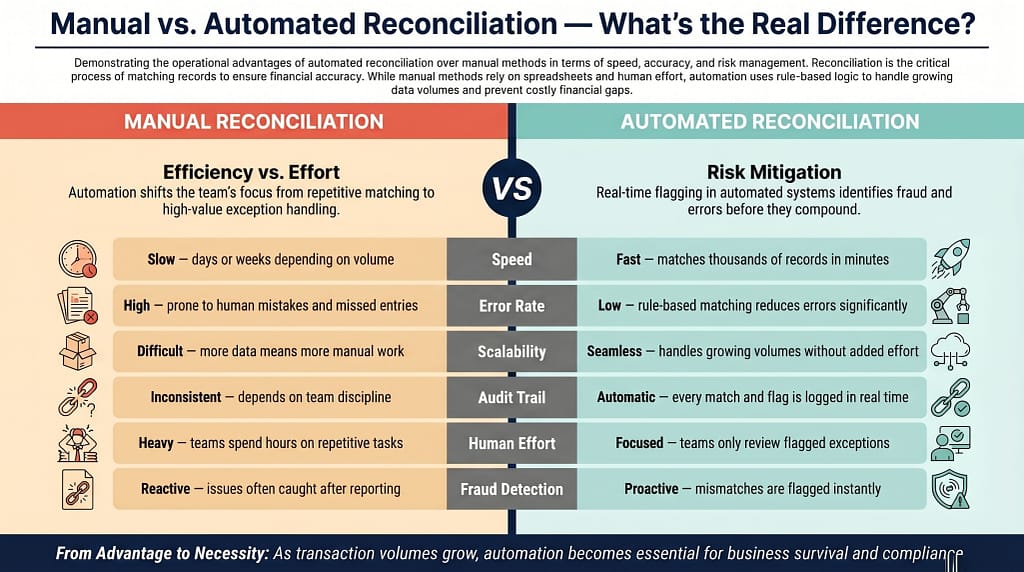

Can reconciliation be automated?

Reconciliation can be automated using software that imports data from multiple systems, matches transactions using rules or AI logic, flags exceptions, and stores complete audit trails. Automation reduces manual work, speeds up close cycles, and improves consistency across large transaction volumes. It also allows teams to focus on investigating real exceptions instead of spending hours on repetitive matching. As businesses grow, automated reconciliation often becomes more efficient than relying only on spreadsheets.

Vapusdata helps businesses automate reconciliation across ERPs, databases, files, and operational systems through governed workflows and faster exception handling. As businesses grow, automated reconciliation often becomes more efficient than relying only on spreadsheets.

Reconciliation with Vapusdata

Manual reconciliation struggles when businesses scale. More systems create more files, more formats, and more exceptions. That is where automation platforms like Vapusdata become valuable.

Based on its product pages, Vapusdata offers reconciliation-focused solutions designed to connect enterprise systems, compare records, identify mismatches, and manage approvals through governed workflows.

In practice, that can include:

- Importing data from ERPs, databases, APIs, and spreadsheets

- Running rule-based or intelligent transaction matching

- Flagging discrepancies instantly

- Sending exceptions for review and approval

- Maintaining logs for audits

- Supporting faster month-end close cycles

This shift matters because reconciliation is no longer only an accounting task. It now supports compliance, reporting quality, and faster decision-making.

Businesses that treat reconciliation as an ongoing process instead of a month-end scramble often build stronger finance operations over time.

Automated Reconciliation reduces manual effort, improves matching speed, and creates better control over exceptions. It also helps teams scale without adding the same level of manual workload.

Reconciliation keeps business numbers honest. It helps teams detect errors early, trust reports, stay compliant, and move faster with confidence. As finance operations become more connected and data-heavy, automated reconciliation will likely shift from a nice-to-have tool to a basic requirement.

FAQs

Reconciliation is the process of checking whether two sets of records match and fixing any differences. Businesses use it to maintain accurate data.

2. Why is reconciliation important?

Reconciliation is important because it catches errors, prevents losses, and improves trust in financial reporting. It also supports audits and tax compliance.

3. What causes reconciliation differences?

Reconciliation differences are caused by timing gaps, duplicate entries, missing transactions, fees, currency issues, or manual mistakes. Poor system integration can also create mismatches.

4. Is reconciliation only for finance?

Reconciliation is not limited to finance. Businesses also reconcile inventory, payroll, taxes, customer data, and operational records across systems

5. What is a Bank reconciliation statement?

A Bank reconciliation statement is a report that explains differences between company bank records and the bank’s official statement. It lists timing gaps, charges, errors, and corrections needed to match balances.

6. Can reconciliation be automated?

Reconciliation can be automated using software that imports data, matches transactions, flags exceptions, and stores audit trails. Automation saves time and improves consistency. Vapusdata offers all these features natively.

7. How often should reconciliation be done?

Reconciliation should be done based on transaction volume and business risk. High-volume cash accounts may need daily checks, while lower-risk accounts may be reviewed weekly or monthly.

8. What is reconciliation in accounting?

Reconciliation in accounting is the process of comparing accounting records with source documents or statements to ensure balances are correct. Common examples include matching ledgers with bank statements, invoices, or subsidiary records.

9. What is GST reconciliation?

GST reconciliation is the process of cross-checking GST returns – particularly GSTR-1, GSTR-3B, and GSTR-2A/2B – to ensure that tax collected, tax paid, and input tax credit (ITC) claimed are all consistent. Mismatches can result in ITC reversals, interest charges, or penalties from tax authorities.